“You must gain control over your money, or the lack of it will forever control you.”

Dave Ramsey

Want to know the best strategy for teaching your O.T. clients about money management? This technique is a simple way to teach individuals with Autism, ADHD, and anxiety how to budget and manage their money.

You will learn the importance of setting financial goals, how emotions drive spending behavior, how to evaluate past financial decisions, and how to create a simple budget to get started. As a female with ADHD, I have found this method efficient for my spending and budgeting.

After learning these money management strategies, you will feel confident helping your clients and inspired to create your budget, giving you financial freedom.

This post is all about money management in Occupational Therapy.

Budgeting and money management can be daunting, so I’d recommend completing these steps over several O.T. sessions.

There are no right or wrong answers to these reflection questions, but it’s a great way to gain insight into behavior and self-awareness.

I’d encourage them to imagine the best-case scenario and respond with their deepest desires to plan for the life they dreamed of.

You don’t have to answer all of these, but here are 18 self-reflection questions to get started:

Emotions drive behavior, which is why it’s essential to understand one’s emotions about money and how they impact spending, saving, and budgeting behaviors.

Here are some emotions commonly felt with money management.

Reassure them that there are no right or wrong answers.

If you are familiar with the Zones of Regulation curriculum, this is an excellent opportunity to incorporate evidence-based practice into the activity.

The Green Zone is when we feel most productive and focused.

For example, some identify as a “morning bird,” “night owl,” or a “permanently exhausted pigeon.”

The Blue Zone is characterized by low energy and moving slowly.

The Yellow Zone occurs when there is some control but energy levels are heightened.

The Red Zone is a sensation of feeling out of control and highly heightened energy levels.

Needs are essential for survival and are necessities to live and work.

Physiological and safety needs are at the bottom of Maslow’s hierarchy of Needs, which indicates that they must be addressed first.

An individual must feel safe and cared for to build a solid foundation for intellectual and creativity.

Wants are not essential for survival but make life more comfortable and enjoyable.

Therefore, wants can be considered splurges and weaknesses.

Individuals with ADHD struggle with impulse control, so it’s crucial to identify and create a plan.

If you or your client struggle with impulse control, DO NOT get a credit card.

Credit cards can be a dangerous cycle brought on by instant gratification and “carefree” spending.

High interest rates (+20%) are one of the significant consequences once the credit card bill arrives in the mail.

After answering the reflection questions honestly, it’s time to identify one financial goal to focus on.

Here is the formula for writing SMART goals:

The three common financial goals are:

Choose one specific money goal that aligns with their desired result.

Thankfully, financial goals are easy to measure and quantify.

However, to make goals measurable, help your client find the exact monthly number and the total end goal.

For example, saving $1,000 a month would be the end, and $100 would be the monthly amount.

Is this financial goal compatible with the individual’s strengths and weaknesses regarding money?

Does it match past money behaviors?

Does the goal align with core values and dreams?

Does it match their current life situation?

This goal should be a step forward toward achieving their financial goals and dream lives.

When is the anticipated date for this financial goal to be achieved?

It could be days, weeks, months, or one year.

For this step, you will need a paper printout of the most recent bank statements and highlighters to color code and categorize.

You don’t have to use these exact colors, F.Y.I.

After color coding each section, add the totals and write them down on paper as you will need the amounts for the next step.

After color-coding the bank statements, it’s time to apply the 50/30/20 rule (you can use Google to double-check accuracy).

There is no shame in using your resources. For example, “What is 20% of $3,500?”

The monthly take-home income is the leftover paycheck after taxes and other payroll deductions (i.e., health insurance and retirement).

To calculate 50% of the income, divide it in half. For example, 50% of a $3,500 monthly income is $1,750.

The following two sections are for the other 50% of the income. For example, 30% of $3,500 is $1,050.

This is the last piece of the income pie. For example, 20% of $3,500 is $700.

The 50/30/20 method doesn’t have to be perfect and exact, but it’s a great starting point.

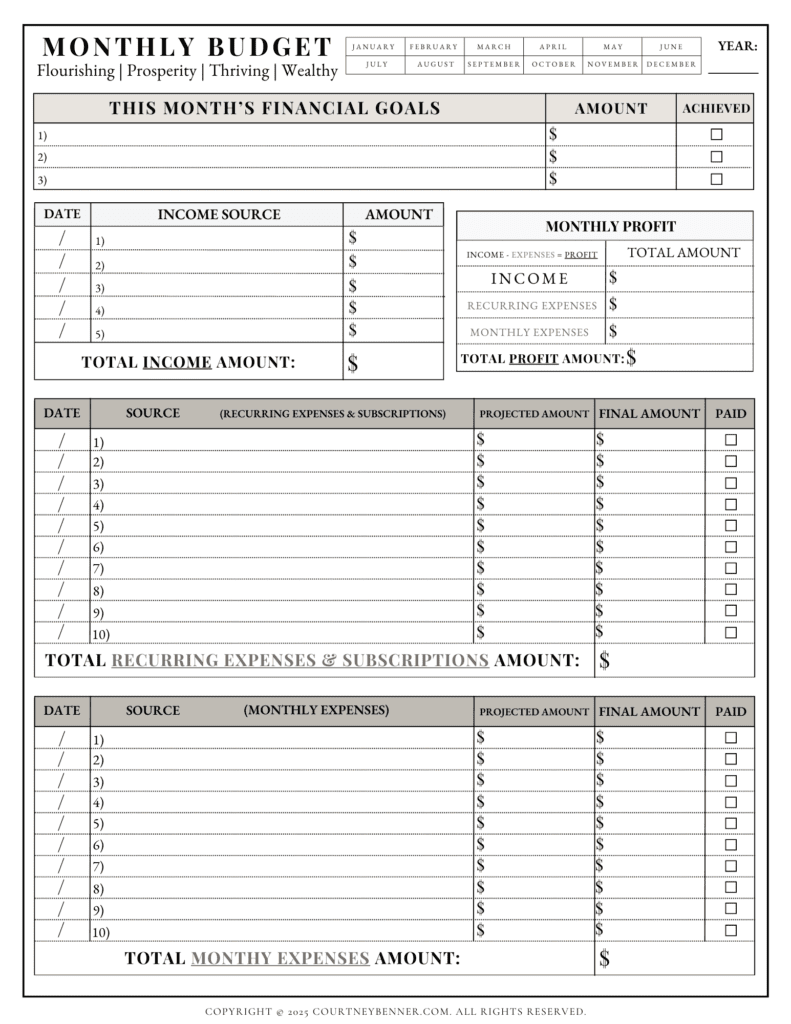

The first step to creating a budget is to list every source of monthly take-home income, which is the leftover paycheck after taxes and other payroll deductions (i.e., health insurance and retirement).

Note: Some employers send paychecks on set dates every month for 24 paychecks per year, and some pay their employees every other week for 26 paychecks per year.

The second step is to write the monthly expenses (needs + wants) using the 50/30/20 rule.

The third step is to identify the due dates. Finally, you can enroll in auto-payments if the client struggles with memory and organization skills.

The fourth step is to subtract the income from the expenses.

The fifth step is to analyze if there is more income than expenses or vice versa.

If there is more income than expenses, the leftover money can go towards the S.M.A.R.T. goal.

If there are more expenses than income, trim the wants list until it balances out to zero.

At the end of the month, you can help the client reflect on how the budget did or did not work for them.

Sign up for my newsletter and receive these FREE printable money management printables for budgeting, paying off debt, and saving money.

© 2025 Courtney benner. all rights reserved.

THIS WEBSITE IS A PARTICIPANT IN THE AMAZON SERVICES LLC ASSOCIATES PROGRAM, AN AFFILIATE ADVERTISING PROGRAM DESIGNED TO PROVIDE A MEANS FOR SITES TO EARN ADVERTISING FEES BY ADVERTISING AND LINKING TO AMAZON.COM.

PRIVACY POLICY

DISCLAIMER POLICY

TERMS AND CONDITIONS

")